20+ Years of Common Sense Investing: Our Top 5 Principles

When we launched the Strategic Income Fund over 20 years ago, we knew we were trying something a little different. Our goal was to create an all-weather bond fund that would effectively act as a one-stop-shop for our private clients, providing a compelling yield without taking on too much risk. We designed the strategy to be flexible so we could invest in the most attractive areas of the market based on economic circumstances and cyclical forces.

Although “go-anywhere” bond funds were relatively uncommon back then, to us the approach seemed somewhat obvious. Common sense dictated that having the ability to invest where we wanted, regardless of credit rating, sector, or maturity, would give us the best chance to create a fixed income portfolio that could do well in any market environment.

Looking back on over two decades of outperformance, we feel our strategy has delivered just as we hoped it would. Our day-to-day decisions have always been informed by a range of factors, but our commitment to our philosophy has never wavered. Below are our top five common sense investment principles.

Do Not Follow the Crowd

When looking for investment opportunities, we have always found it is better to focus on areas of the market that are somewhat under the radar. We prefer to invest in lesser-known companies and use our thorough due diligence process to determine whether they are a good fit for our portfolio. Likewise, we do not place too much emphasis on credit ratings, as they tend to be backward-looking and can be slow to reflect improving fundamentals. In general, our goal is to find companies with durable business models and solid financials.

Similarly, we are selective when it comes to securities that are included in fixed income indexes. These bonds have typically been in high demand by both passive managers and active managers who closely follow their respective benchmarks, so the issuers have less incentive to offer favorable terms. Our flexible mandate affords us the luxury of focusing only on the subset of index securities that we feel are attractive.

Cash is Critical

This is our version of the old adage “cash is king.” In our view, cash is a tactical asset that provides multiple important benefits, and it is an essential component of our strategy. In general, our cash allocation has increased during periods of market volatility and decreased when conditions are calm.

For us, cash is most helpful during periods of market distress, as this is an excellent time to hunt for bargains. When other managers experience redemptions, they may be forced to liquidate positions to cover outflows. Our cash has allowed us to take advantage of these opportunities without having to sell any of our own portfolio (as well as cover any outflows we may experience). As a result, some of our best performing bonds have been purchased during selloffs, when we have been able to acquire high quality securities at discount prices. These bonds have also tended to recover relatively quickly once markets stabilize, which can translate into stronger returns.

Our cash position may reduce both our volatility and our duration. Our larger allocation during periods of uncertainty has provided us with a buffer should conditions worsen, as our cash is able to offset some of the unrealized losses from our bond portfolio. We also generally increase our cash allocation in periods of rising rates and peaking fundamentals, which decreases our duration and can potentially help reduce our losses when markets reverse gear.

Do Not Stretch

One of the most important principles of our approach is that we prefer to accept what the market has on offer, which can result in receiving slightly less yield in rising markets in order to reduce our downside in falling markets. In practical terms, this means we will not stretch for yield either by going down in credit quality or buying longer maturities unless we feel the additional return justifies locking up our capital for a longer period.

We take a particularly cautious approach to credit risk. Much of our portfolio is invested in bonds that are below investment grade, so due diligence is critical to our success. We make every effort to verify that the companies in our portfolio are robust, profitable businesses, and if we are not satisfied with the business model, execution, or capital allocation decisions, we will not invest, even if a bond is offering a yield that is well above market rates. Discipline is key, as the cost of owning a bond with deteriorating fundamentals can add up quickly – the value of the security declines as the business struggles, and things can turn from bad to worse if the bond is downgraded or defaults.

We are similarly cautious with our duration profile. Like most managers, we tend to shorten our duration during periods of rising rates, but we feel it also makes sense to shorten duration in the following situations:

- When the yield curve is flat – If we are not getting paid more to commit our capital for longer, we stick with shorter maturity bonds.

- When markets are uncertain – If markets are in a precarious state, we prefer to have shorter-term bonds in our portfolio, as they mature more quickly, giving us the option to either reinvest or increase our cash allocation.

We realize that shortening our duration reduces our upside should the market enjoy an extended rally, but we gladly make that tradeoff when we are not confident in its trajectory. Of course, when we are bullish, and we have an opportunity to acquire quality securities at attractive prices, we will act aggressively, buying longer-dated bonds because it makes sense to lock up higher yields for as long as possible when bonds appear cheap.

Ensure Lender and Borrower Incentives Are Aligned

When considering individual bonds for our portfolio, we have always found that we achieve the best outcomes when we invest in companies that are responsible stewards of capital. We have a strong preference for owners and executives who are transparent and who use bond proceeds to invest directly in the growth of the business. These types of issuers are usually public companies or are family-owned and are committed to a long-term vision. They understand that maintaining good relationships with their creditors will help them in the long run.

As part of our research process, we also look carefully at each issuer’s capital structure and bond covenants to make sure they possess the necessary financial resources to execute their long-term vision and that our interests are protected should their priorities change. We are looking for companies with sufficient capital to both operate and expand their business, and as a result, routinely generate free cash flow. We also want to be sure our issuers do not carry an excessive debt burden, as even a profitable company that is overleveraged will struggle to repay its debts.

At the opposite end of the spectrum, we actively avoid issuers who use bond proceeds for either shareholder dividends or stock buybacks. These types of issuers are frequently private equity owned companies who raise funds for leveraged buyouts. Generally, the incentives between the issuers and the borrowers are misaligned, as these owners are primarily focused on extracting as much cash from the companies with debt-financed dividends as quickly as possible and are much less concerned about what the high debt load will do to the company’s fortunes.

Focus on the Most Attractive Areas of the Market

Our final principle is that it is important to remain nimble and focus on areas of the market where the risk/return tradeoff is most favorable. In our experience, the best way to respond to shifting market conditions is to rotate into areas that are offering attractive compensation relative to their risk.

Our flexible approach allows us to invest across markets regardless of credit rating, sector, or maturity, and we utilize that freedom to build a diverse portfolio of quality bonds. We try to identify the most attractive parts of the market, whether that is a sector or industry, and then seek to invest in a manner that skews the risk/reward most asymmetrically in our favor. That may not always result in owning the highest yielding bonds (see “Do Not Stretch” above).

In addition, we have the ability to invest in areas of the market that may be more prone to inefficiency, such as convertible bonds. These securities possess attributes of both bonds and stocks, and many managers do not have the expertise to analyze them or the industry contacts to trade them. Given our multiple decades of experience working with convertibles, we have both, and they are an integral part of our strategy. Over the years, they have been some of our best performing positions.

The Result: A Track Record We Are Proud Of

The world has changed a lot since we launched the fund over 20 years ago, but common sense is timeless. By sticking to basic principles, we have been able to consistently outperform our benchmark for two decades without taking on materially more risk.

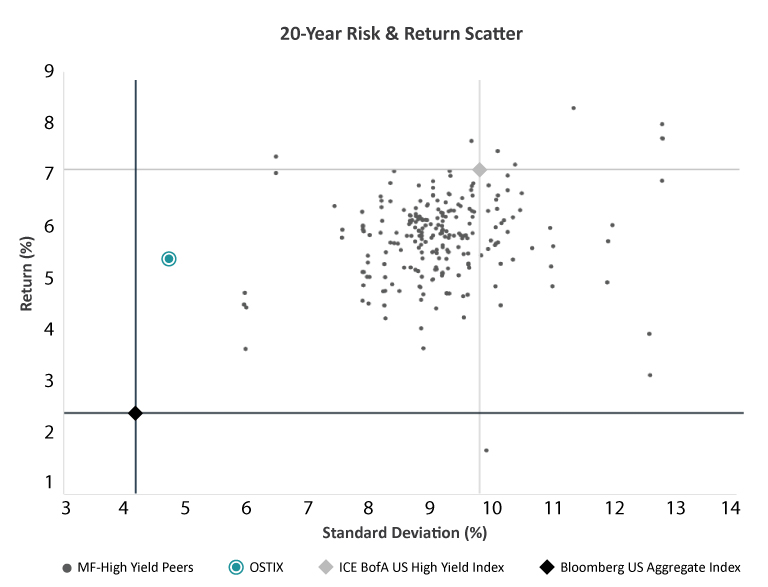

Outperformance with Limited Downside

The chart below provides a visual representation of how we have performed versus the investment grade index, the high yield index, and the Lipper universe of high yield active managers. (We feel it is meaningful to look at performance relative to high yield as our strategy tends to focus more on that area of the market.) There are three key takeaways:

- Our returns are significantly higher than the investment grade index, but our risk (standard deviation) is only marginally higher.

- Our returns are comparable to those of the high yield index, but our risk is substantially lower.

- Compared to the Lipper universe of high yield bond funds, our risk is well below all the other managers, while our return is roughly in the midpoint of that universe.

In our view, this chart clearly demonstrates that although we have been willing to sacrifice some upside in order to protect on the downside, we have still been able deliver strong returns and outperform our benchmark.

Source: eVestment. Reflects database updates through 9/30/2023, 149 Lipper High Yield peer group members reporting 20-year returns.

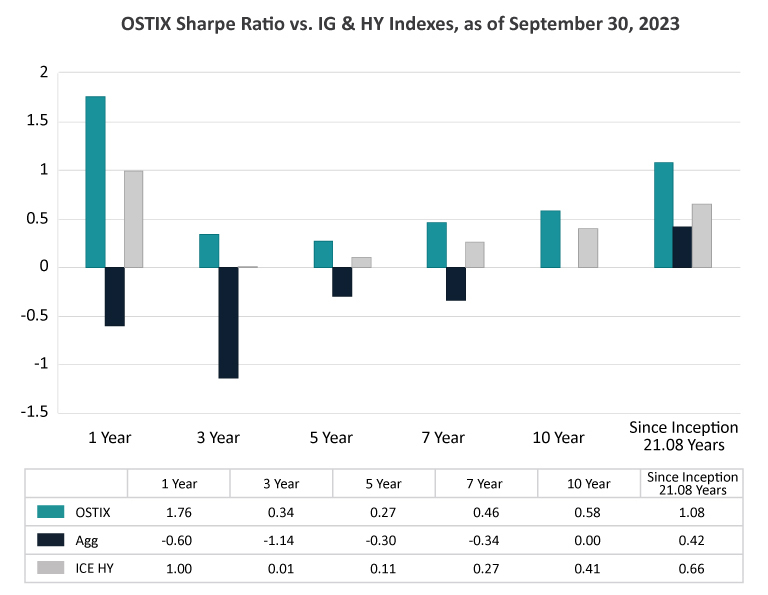

Higher Sharpe Ratios

The next chart shows our Sharpe Ratio versus both the investment grade and high yield indexes across time. The Sharpe Ratio measures risk-adjusted returns (higher is better)1. Investors can use Sharpe Ratios to compare funds and assess whether their returns are worth the risk they are adding to their portfolio.

As you can see, our fund has delivered a significantly higher Sharpe Ratio than both indexes in nearly every period shown below. In our view, this is perhaps the single strongest argument in favor of our approach. We set out to create a product that could outperform the investment grade index without taking substantially more risk, and this chart indicates that we have achieved our goal thus far.

Source: eVestment. Inception date is 8/30/2002.

Final Thoughts

Although our approach is based on common sense, it requires hard work and discipline to execute. After over 20 years, we have the same passion and enthusiasm we had on day one, and we do not see that changing anytime soon. The past few years have been a wild time in the fixed income markets, highlighted by the pandemic, inflation, and the Fed’s current tightening cycle, and we feel our philosophy is as relevant today as it was two decades ago.

This piece was originally published on September 7, 2022.

1The numerator of the Sharpe Ratio is the difference between a fund’s return and the risk-free rate, and the denominator is the fund’s volatility as measured by standard deviation.

Carl Kaufman

CIO – Strategic Income & Managing Director – Fixed Income

Craig Manchuck

Vice President & Portfolio Manager – Strategic Income

Bradley Kane

Vice President & Portfolio Manager – Strategic Income

Featuring

Carl Kaufman

CIO – Strategic Income & Managing Director – Fixed Income

Carl Kaufman has managed the Osterweis Strategic Income Fund since its inception and serves as the Managing Director of Fixed Income, as well as a Portfolio Manager for the Osterweis Growth & Income strategy. He is also a member of the firm’s Management Committee.

He joined Osterweis Capital Management in 2002, after nearly 24 years at Robertson Stephens and Merrill Lynch.

Carl graduated from Harvard University and attended New York University Graduate School of Business Administration.

Outside his professional endeavors, he enjoys playing classical piano and actively contributes to the community as a member of the Board of Trustees for the San Francisco Conservatory of Music, supporting the arts and enhancing the cultural fabric of the SF Bay Area. Additionally, he enjoys playing golf, an activity that continually challenges his patience and precision.

Craig Manchuck

Vice President & Portfolio Manager – Strategic Income

Craig Manchuck, a partner at Osterweis, is a Portfolio Manager for the strategic income strategy. In this role he enjoys investing clients’ assets in a common sense way that is designed to generate good risk-adjusted returns. Throughout his career, Craig has learned the importance of patience and that relationships with company management teams are invaluable.

Prior to joining Osterweis Capital Management in 2017, Craig was a Managing Director of Fixed Income Sales at Stifel Nicolaus, where he was responsible for sales and origination of high yield bonds, leveraged loans, and post reorg equities. Before Stifel, he held a similar role at Knight Capital. Before that, Craig was the Executive Director for Convertible Securities and then High Yield/Distressed Securities at UBS. He has previous experience in Convertible Securities Sales at Donaldson, Lufkin & Jenrette, SBC Warburg, and Merrill Lynch.

Craig graduated from Lehigh University with a B.S. in Finance and NYU Stern School of Business with an M.B.A. Outside of work, he enjoys golfing, wine, gardening, and spending time with family.

Bradley Kane

Vice President & Portfolio Manager – Strategic Income

Bradley (Brad) Kane is a Portfolio Manager for the strategic income strategy and a partner at the firm. In his role he leverages his extensive experience and deep understanding of the market to seek out opportunities to deliver clients attractive risk-adjusted returns.

Prior to joining Osterweis in 2013, Brad was a Portfolio Manager and Analyst at Newfleet Asset Management, where he managed both high yield and leveraged loan portfolios. Before that, he was a Vice President at GSC Partners, focusing on management of high yield and collateralized debt obligations. Earlier in his career, he managed high yield assets as a Vice President at Mitchell Hutchins Asset Management. In these positions he learned the importance of staying focused on one’s investing strategy and discovering new securities and investor types without succumbing to trends.

Brad graduated from Lehigh University with a B.S. in Business & Economics. Outside of his professional life, he enjoys playing golf and ice hockey, as well as indulging in his diverse taste in music, including a particular appreciation for heavy metal.

For more information about this strategy, please send us an email or call us at (800) 700-3316.

Opinions expressed are those of the authors, are subject to change at any time, are not guaranteed and should not be considered investment advice.

Standardized performance is available here.

Performance data quoted represent past performance; past performance does not guarantee future results. The investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance of the Fund may be higher or lower than the performance quoted. Performance data current to the most recent month end may be obtained by calling (866) 236-0050. An investment should not be made solely on returns. The Fund’s gross expense ratio was 0.84% as of March 31, 2022.

Mutual fund investing involves risk. Principal loss is possible. The Osterweis Strategic Income Fund may invest in debt securities that are un-rated or rated below investment grade. Lower-rated securities may present an increased possibility of default, price volatility or illiquidity compared to higher-rated securities. The Fund may invest in foreign securities, which involve greater volatility and political, economic and currency risks and differences in accounting methods. Investments in debt securities typically decrease in value when interest rates rise. This risk is usually greater for longer-term debt securities. Small- and mid-capitalization companies tend to have limited liquidity and greater price volatility than large-capitalization companies. From time to time, the Fund may have concentrated positions in one or more sectors subjecting the Fund to sector emphasis risk.

The Bloomberg U.S. Aggregate Bond Index (Agg) is widely regarded as a standard for measuring U.S. investment grade bond market performance.

ICE BofA U.S. High Yield Index tracks the performance of U.S. dollar denominated below-investment grade corporate debt publicly issued in the U.S. domestic market.

Lipper’s High Yield Funds classification includes funds that aim at high (relative) current yield from fixed income securities, have no quality or maturity restrictions, and tend to invest in lower-grade debt issues.

Indices cited do not incur expenses and are not available for investment. These indices reflect the reinvestment of dividends and/or interest. Historical fixed income index data is provided for informational purposes only, not as an indication of future Fund performance.

Duration measures the sensitivity of a fixed income security’s price (or the aggregate market value of a portfolio of fixed income securities) to changes in interest rates. Fixed income securities with longer durations generally have more volatile prices than those of comparable quality with shorter durations.

The Sharpe Ratio represents the added value over the risk-free rate per unit of volatility risk.

Standard Deviation is a measure of dispersion that represents the degree to which an investment’s returns vary around a mean. The greater the Standard Deviation, the more volatile an investment’s returns were during the period measured. This statistic is calculated using the population standard deviation formula: Standard Deviation = Square root of [(Sum of squared deviations from mean)/(Number of returns in the period measured)] If the return periodicity is less than one year, the standard deviation is multiplied by the square root of the number of periods in one year in order to arrive at an annualized measure.

Free cash flow represents the cash that a company is able to generate after laying out the money required to maintain and expand the company’s asset base. Free cash flow is important because it allows a company to pursue opportunities that enhance shareholder value.

The Osterweis Funds are available by prospectus only. The Funds’ investment objectives, risks, charges, and expenses must be considered carefully before investing. The summary and statutory prospectuses contain this and other important information about the Funds. You may obtain a summary or statutory prospectus by calling toll free at (866) 236-0050, or by visiting www.osterweis.com/statpro. Please read the prospectus carefully before investing to ensure the Fund is appropriate for your goals and risk tolerance.

Osterweis Capital Management is the adviser to the Osterweis Funds, which are distributed by Quasar. [OCMI-462695-2023-11-29]