Dividend Growth Stocks and High Yield Bonds: An Innovative Approach to Generating Investment Income

Generating investment income is an age-old challenge that has been particularly difficult recently, as bond yields have been stubbornly low since the Great Financial Crisis. Creating consistent cashflow is a top priority not only for retirees, but also for endowments, foundations, and family offices that need to fund their operations. For many investors (and their advisors), the standard playbook is to increase their fixed income allocation and reduce their equity allocation, creating a reliable cashflow stream and decreasing portfolio volatility.

The downside of this approach is that it makes it harder for portfolios to grow, as investors are spending (rather than reinvesting) the proceeds from their fixed income investments. At the same time, they are dipping into their equity portfolio to cover any shortfalls or unexpected expenses. The combination can result in a portfolio with both declining principal and income potential.

In managing assets for both high-net-worth individuals and institutions for nearly 40 years, we have found that a dividend growth strategy, which invests in the subset of dividend-paying stocks with growing earnings and dividends, combined with an allocation to shorter-term non-investment grade bonds is a compelling solution to this problem. It provides a combination of relatively high current income, future income growth, and capital appreciation, while still limiting volatility.

Dividend-Paying Stocks Are Diverse

Despite its reputation as a haven for antiquated, stodgy companies, the dividend-paying universe is fairly diverse, with over 75% of the S&P 500 paying dividends. Although many dividend-paying stocks fit the traditional stereotype – mature businesses with above-average yields and slow growth rates – there are also plenty of dividend growth stocks – dynamic companies that operate in expanding markets with favorable long-term growth prospects.

We feel that investors with a multi-year time horizon are far better off holding dividend growth stocks than slower growing stocks with a higher dividend payout. In the short run, dividend growth stocks may produce slightly less income, as they generally offer lower payout rates, but over time their faster top-line growth should provide investors with compound returns in both their income stream and their share price appreciation.

Dividend-Paying Stocks Perform Better in Down Markets

Another benefit of dividend-paying stocks is that they tend to perform better in difficult markets than stocks that do not pay a dividend. This makes sense because investors gravitate toward profitable companies when sentiment turns bearish, especially those that return a portion of their free cashflow directly to shareholders.

According to a recent research note from Credit Suisse, this is exactly what has happened since the onset of the pandemic:

“Companies that are returning more of their excess capital to shareholders in the form of dividends are continuing to see incredibly strong performance. This is in contrast to buybacks, which are often viewed by market participants as a driver of share prices.”

Dividend growth companies fared particularly well during the latest market selloff. In the past year, the S&P 500 Dividend Aristocrats Index has lost only -3.68%, compared to a much more substantial -10.62% loss for the broader S&P 500.

This feature is especially relevant today, given the current market volatility and the ongoing uncertainty in the economy. Of course, dividend-paying stocks can still decline in bear markets, and in extreme cases they can even skip a scheduled dividend payment, but their higher degree of profitability can provide protection in turbulent times.

Shorter-Term High Yield Bonds Are an Effective Complement

In our view, shorter-term high yield bonds pair particularly well with dividend growth stocks as part of an income generating strategy. They have two primary benefits. First, they dampen overall portfolio volatility. A pure dividend growth equity strategy might have more upside, but it also has substantially more downside. Layering in a fixed income buffer can help reduce drawdowns.

The second benefit is that they generally offer larger yields than dividend stocks, thus increasing current income. We particularly like shorter duration high yield bonds, as their coupons are higher than their investment grade counterparts. Their higher yields also translate into less interest rate risk than investment grade bonds of comparable maturity. (Interest rate risk, also known as duration, decreases as maturities fall and yields rise.) Likewise, they have less credit risk than similarly rated longer maturity issues, as the bondholder is exposed to the borrower for a shorter period of time.

Our Philosophy in Practice

Our views about generating investment income have been shaped by decades of helping both individuals and institutions reach their long-term financial goals. In our experience, the best outcomes occur when investors are able to position their portfolios to generate growing income streams without sacrificing capital appreciation or taking on too much risk. To help our clients achieve this, we have developed the Growth & Income Fund, which utilizes a flexible combination of our favorite dividend growth stocks with a selection of shorter-term non-investment grade bonds.

Stocks: Industry Leaders and Secular Growers

We believe the best way to deliver strong long-term performance is to build an equity portfolio of attractively valued stocks issued by leading or dominant companies in their respective industries. These firms are generally able to gain market share over time and enjoy higher margins. This enables them to grow revenues and free cash flow, which allows them to raise dividends faster than their competitors. Additionally, they are typically more durable and hence can be owned for many years, improving the tax efficiency of our strategy.

We also look for companies that benefit from secular tailwinds – firms that are selling products and services in sectors of the economy that are undergoing structural growth. Currently we are focusing on several areas, including the shift away from carbon-based fuels to alternative energy, the shift toward electric vehicles, the shift from brick-and-mortar retail to e-commerce, and the digitization of the economy, to name a few. We believe these sectors should grow over the long term, regardless of the business cycle, and the individual companies should be able to grow faster than the overall market.

Bonds: A Steady Source of Income

We supplement the income from our equities with a carefully selected portfolio of mostly shorter-duration high yield bonds. We emulate the philosophy of our Strategic Income fund within our fixed income allocation, which means we are always looking for the areas of the market that have the most attractive risk/reward characteristics, regardless of credit rating, sector, or maturity. At the same time, we are careful not to stretch for yield, which reduces our losses in weak markets.

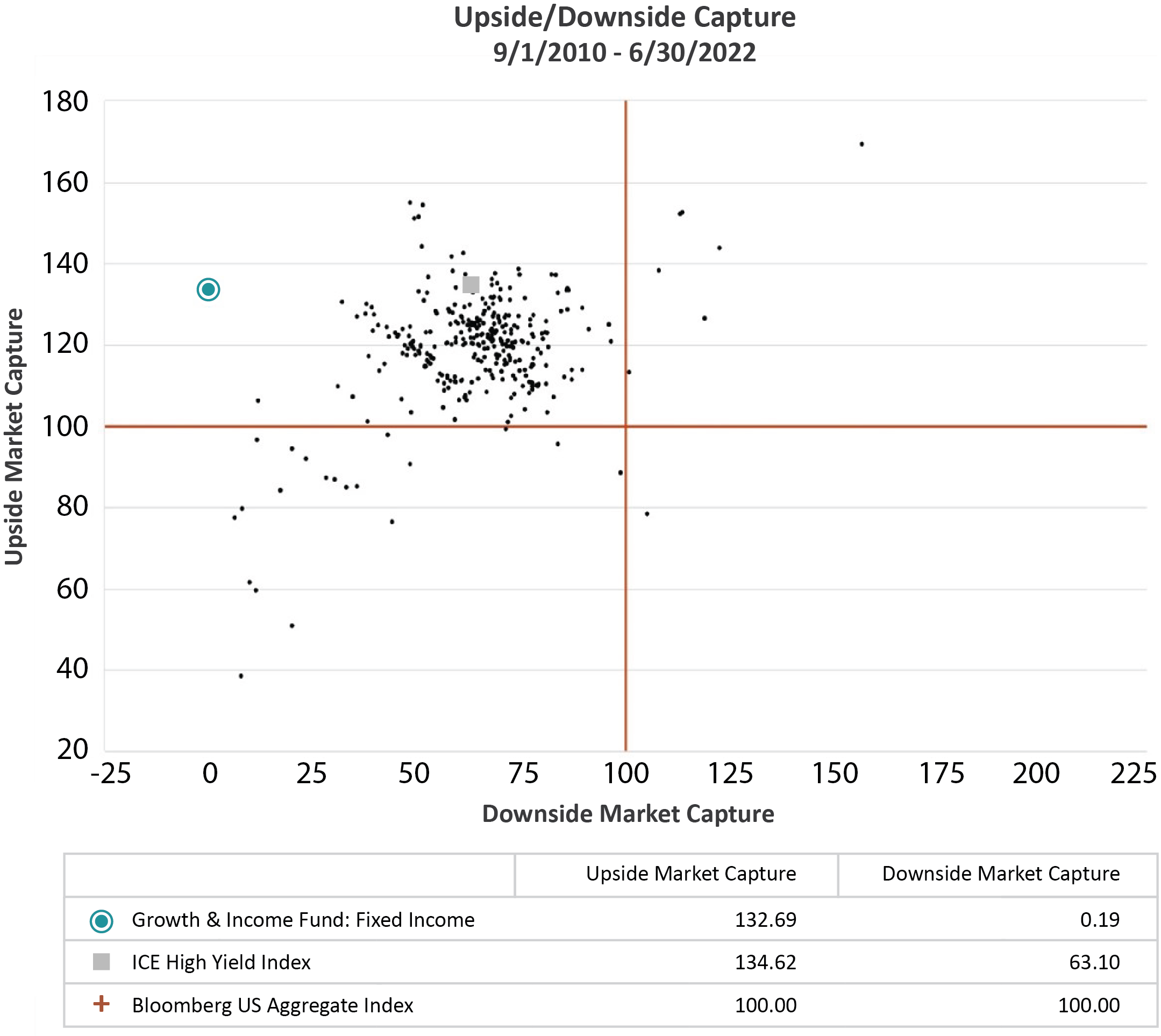

As you can see from the scatterplot below, we have been successful with this approach. The x-axis plots the downside capture ratio , which measures how an investment performs during falling markets. A lower number is better, as it indicates the portfolio is less correlated with changes in the market. The y-axis plots the upside capture ratio, which of course is the opposite, and a higher number is better.

Source: eVestment

Since inception, the downside capture of the fixed income portion of the Growth & Income Fund is decidedly lower than both the high yield index and every high yield bond fund in the Lipper universe. At the same time, the upside capture is near the top of the peer group and almost identical to the high yield index.

Final Thoughts

Although no single portfolio is appropriate for everyone, we believe that most income-seeking investors would benefit from maintaining at least some exposure to dividend growth stocks and shorter-term high yield bonds. At Osterweis, we offer the Growth & Income Fund, which seeks to provide a combination of current income, future income growth, and capital appreciation.

1The Dividend Aristocrat Index is a subset of the S&P 500 that is made up of companies that have increased their dividend every year for at least 25 consecutive years.

2The downside market capture ratio is calculated by dividing the portfolio’s return when the benchmark (Bloomberg U.S. Aggregate) performance is negative by the return of the benchmark during the same periods.

3The upside market capture ratio is calculated by dividing the portfolio’s return when the benchmark (Bloomberg U.S. Aggregate) performance is positive by the return of the benchmark during the same periods.

John Osterweis

Founder, Chairman & Co-Chief Investment Officer – Core Equity

Carl Kaufman

CIO – Strategic Income & Managing Director – Fixed Income

Featuring

John Osterweis

Founder, Chairman & Co-Chief Investment Officer – Core Equity

John Osterweis founded Osterweis Capital Management to serve the portfolio needs of high-net-worth investors, foundations, and endowments. He is currently Chairman of the firm as well as a member of the firm’s Management Committee and a Portfolio Manager for the core equity, growth & income, and flexible balanced strategies.

After graduating from business school, John served as a Senior Analyst concentrating on the forest products and paper industry for several regional brokerage firms and later for E.F. Hutton & Company, Inc. In addition to his activities as an analyst, John served as Director of Research for two firms and managed equity portfolios for over ten years. In late 1982, John decided to devote himself full time to his portfolio management activities, and in April of 1983 launched Osterweis Capital Management.

John graduated from Bowdoin College (B.A. in Philosophy, cum laude), and Stanford Graduate School of Business (M.B.A. with top honors in Finance).

Outside of his work, John is an active supporter of our community. He has served as Director of the Lucas Museum of Narrative Art, Director on the Stanford Alumni Association Executive Board, Trustee of Bowdoin College, Director and Vice Chairman of Mt. Zion Hospital and Medical Center, and President of the Board of Directors for Summer Search Foundation. He currently serves as a Trustee of the San Francisco Ballet Association, Director of the San Francisco Free Clinic, and President Emeritus of the San Francisco Ballet Endowment Foundation, as well as Trustee Emeritus of Summer Search Foundation and of Bowdoin College. He also enjoys horseback riding and other outdoor activities.

Carl Kaufman

CIO – Strategic Income & Managing Director – Fixed Income

Carl Kaufman has managed the Osterweis Strategic Income Fund since its inception and serves as the Managing Director of Fixed Income, as well as a Portfolio Manager for the Osterweis Growth & Income strategy. He is also a member of the firm’s Management Committee.

He joined Osterweis Capital Management in 2002, after nearly 24 years at Robertson Stephens and Merrill Lynch.

Carl graduated from Harvard University and attended New York University Graduate School of Business Administration.

Outside his professional endeavors, he enjoys playing classical piano and actively contributes to the community as a member of the Board of Trustees for the San Francisco Conservatory of Music, supporting the arts and enhancing the cultural fabric of the SF Bay Area. Additionally, he enjoys playing golf, an activity that continually challenges his patience and precision.

For more information about this strategy, please send us an email or call us at (800) 700-3316.

Related Insights

Growth & Income Fund Quarter-End Performance (as of 6/30/26)

| Fund | 1 MO | QTD | YTD | 1 YR | 3 YR | 5 YR | 10 YR | 15 YR |

INCEP (8/31/2010) |

|---|---|---|---|---|---|---|---|---|---|

| OSTVX | 1.16% | 8.07% | 5.77% | 11.74% | 11.32% | 6.12% | 9.04% | 8.37% | 9.09% |

| 60% S&P 500 Index/40% Bloomberg U.S. Aggregate Bond Index | -0.47% | 9.31% | 6.45% | 14.76% | 13.92% | 8.10% | 9.98% | 9.62% | 10.17% |

| S&P 500 Index | -0.95% | 15.20% | 10.21% | 22.32% | 20.61% | 13.41% | 15.51% | 14.36% | 15.34% |

| Bloomberg U.S. Aggregate Bond Index | 0.24% | 0.67% | 0.62% | 3.79% | 4.16% | 0.08% | 1.54% | 2.28% | 2.25% |

Gross expense ratio as of 3/31/26: 0.98%

Performance data quoted represent past performance; past performance does not guarantee future results. The investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance of the Fund may be higher or lower than the performance quoted. Performance data current to the most recent month end may be obtained by calling shareholder services toll free at (866) 236-0050.

Rates of return for periods greater than one year are annualized.

Where applicable, charts illustrating the performance of a hypothetical $10,000 investment made at a Fund’s inception assume the reinvestment of dividends and capital gains, but do not reflect the effect of any applicable sales charge or redemption fees. Such charts do not imply any future performance. During the period noted, fee waivers or expense reimbursements were in effect for the Growth & Income Fund.

Source for any Bloomberg index is Bloomberg Index Services Limited. BLOOMBERG® is a trademark and service mark of Bloomberg Finance L.P. and its affiliates (collectively “Bloomberg”). Bloomberg owns all proprietary rights in the Bloomberg Indices. Bloomberg does not approve or endorse this material, or guarantees the accuracy or completeness of any information herein, or makes any warranty, express or implied, as to the results to be obtained therefrom and, to the maximum extent allowed by law, neither shall have any liability or responsibility for injury or damages arising in connection therewith.

The 60/40 blend is composed of 60% S&P 500 Index (S&P) and 40% Bloomberg U.S. Aggregate Bond Index (Agg) and assumes monthly rebalancing. The S&P is widely regarded as the standard for measuring large cap U.S. stock market performance. The Agg is widely regarded as a standard for measuring U.S. investment grade bond market performance. These indices do not incur expenses and are not available for investment. These indices include reinvestment of dividends and/or interest income.

References to specific companies, market sectors, or investment themes herein do not constitute recommendations to buy or sell any particular securities.

There can be no assurance that any specific security, strategy, or product referenced directly or indirectly in this commentary will be profitable in the future or suitable for your financial circumstances. Due to various factors, including changes to market conditions and/or applicable laws, this content may no longer reflect our current advice or opinion. You should not assume any discussion or information contained herein serves as the receipt of, or as a substitute for, personalized investment advice from Osterweis Capital Management.

Complete holdings of all Osterweis mutual funds (“Funds”) are generally available ten business days following quarter end. Holdings and sector allocations may change at any time due to ongoing portfolio management. Fund holdings as of the most recent quarter end are available here: Growth & Income Fund

Opinions expressed are those of the authors, are subject to change at any time, are not guaranteed and should not be considered investment advice.

Standardized performance is available here.

Performance data quoted represent past performance; past performance does not guarantee future results. The investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance of the Fund may be higher or lower than the performance quoted. Performance data current to the most recent month end may be obtained by calling (866) 236-0050. An investment should not be made solely on returns. The Fund’s gross expense ratio was 0.97% as of March 31, 2022.

Mutual fund investing involves risk. Principal loss is possible. The Osterweis Growth & Income Fund may invest in small- and mid-capitalization companies, which tend to have limited liquidity and greater price volatility than large-capitalization companies. The Fund may invest in foreign and emerging market securities, which involve greater volatility and political, economic and currency risks and differences in accounting methods. These risks may increase for emerging markets. The Fund may invest in debt securities that are un-rated or rated below investment grade. Lower-rated securities may present an increased possibility of default, price volatility or illiquidity compared to higher-rated securities. Investments in debt securities typically decrease in value when interest rates rise. From time to time, the Fund may have concentrated positions in one or more sectors subjecting the Fund to sector emphasis risk. Investments in asset-backed and mortgage-backed securities include additional risks that investors should be aware of such as credit risk, prepayment risk, possible illiquidity and default, as well as increased susceptibility to adverse economic developments.

The Bloomberg U.S. Aggregate Bond Index (Agg) is widely regarded as a standard for measuring U.S. investment grade bond market performance.

ICE BofA U.S. High Yield Index tracks the performance of U.S. dollar denominated below-investment grade corporate debt publicly issued in the U.S. domestic market. This index reflects transaction costs.

The S&P 500 Index is an unmanaged index that is widely regarded as the standard for measuring large-cap U.S. stock market performance.

Indices cited do not incur expenses unless otherwise noted and are not available for investment. These indices reflect the reinvestment of dividends and/or interest. Historical fixed income index data is provided for informational purposes only, not as an indication of future Fund performance.

Coupon is the interest rate paid by a bond. The coupon is typically paid semiannually.

Duration measures the sensitivity of a fixed income security’s price (or the aggregate market value of a portfolio of fixed income securities) to changes in interest rates. Fixed income securities with longer durations generally have more volatile prices than those of comparable quality with shorter durations.

Free cash flow represents the cash that a company is able to generate after laying out the money required to maintain and expand the company’s asset base. Free cash flow is important because it allows a company to pursue opportunities that enhance shareholder value.

Investment grade bonds are those with high and medium credit quality as determined by ratings agencies.

Yield is the income return on an investment, such as the interest or dividends received from holding a particular security.

The Osterweis Funds are available by prospectus only. The Funds’ investment objectives, risks, charges, and expenses must be considered carefully before investing. The summary and statutory prospectuses contain this and other important information about the Funds. You may obtain a summary or statutory prospectus by calling toll free at (866) 236-0050, or by visiting www.osterweis.com/statpro. Please read the prospectus carefully before investing to ensure the Fund is appropriate for your goals and risk tolerance.

Osterweis Capital Management is the adviser to the Osterweis Funds, which are distributed by Quasar Distributors, LLC. [OSTE-20220913-0592]