Focus on Dividend Growth, Not Dividend Yield

Back to Basics

As part of our Quality Growth approach to equity investing, we tend to gravitate towards companies that pay growing cash dividends and have a long history of doing so. This is because companies that pay stable and growing dividends often can do so because of a durable competitive advantage that enables a long runway of profitable growth. These companies also exhibit healthy underlying fundamentals throughout the economic cycle, generate robust cash flow, and maintain sound balance sheets. And companies that care about sustainably growing cash dividends tend to have boards and management teams that think about the long term with an eye towards preserving and prudently growing cash flows over time.

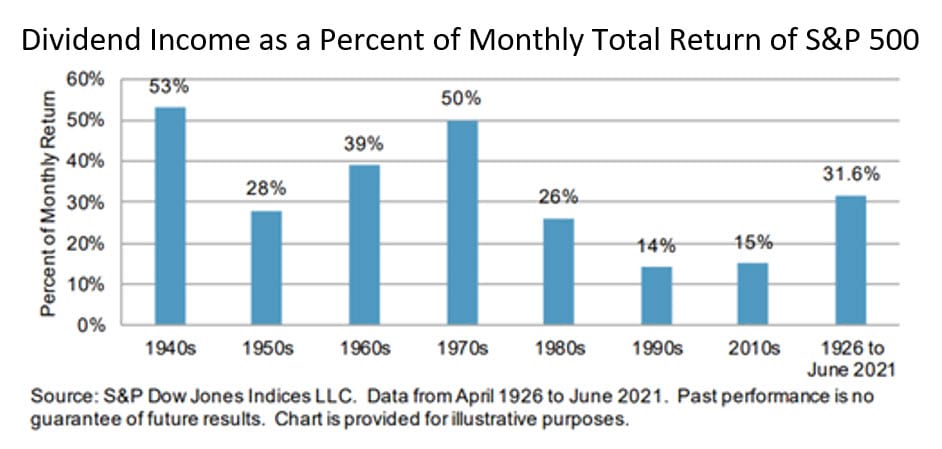

Historically, dividends have played an important role in overall shareholder returns. In fact, a study from S&P Global demonstrates that 32% of shareholder returns in the S&P 500 were generated by dividends from 1926 through June 2021. In some periods, when markets swoon, dividends account for 50% or more of overall S&P 500 returns, as was the case in the three decades of the 1940s, 1970s, and 2000s.

An important element in the contribution of returns from dividends stems from the reinvestment of the dividends, generating incremental compounding that can be very powerful over time.

We Emphasize Growth of Dividends and Focus Less on Yield

It is important to emphasize that we do not just seek companies that pay significant dividends. In fact, our companies often pay out as little as 10-30% of their annual free cash flow generation in the form of dividends. Dividend growth companies tend to retain significant cash flow for reinvestment, perhaps in the form of future acquisitions, which can drive future growth in cash flows. This cash flow growth in turn enables future dividend growth. And leaving room for opportunistic share repurchase can enable very powerful shareholder value creation over time.

We believe a long runway for sustainable growth in free cash flow is the critical element, not the payment of large dividends today. Companies that can sustainably grow their dividends tend to benefit from secular industry tailwinds, pricing power, and/or recurring demand growth. These are exactly the types of businesses we have always sought to invest in, particularly when we catch them at an attractive valuation and/or an inflection point.

Companies that pay out all of their free cash in the form of dividends may carry a high dividend yield that looks attractive at first glance. However, this means the company either has no opportunity to reinvest to drive future growth and thus is in cash harvest mode or will have to use outside capital to reinvest or repurchase shares. Thus, counterintuitively, high dividend yield stocks may often signal problems ahead, while low dividend payors with the ability to grow dividends may be much more attractive.

By selecting companies that both have long histories of paying dividends and growing these dividends annually, we seek to capture the best of both “value” and “growth” investing. These companies have sustainable and enduring growth, but they generate cash flow in excess of their reinvestment opportunities. Over time, this combination can be extraordinarily powerful and significantly benefit portfolios.

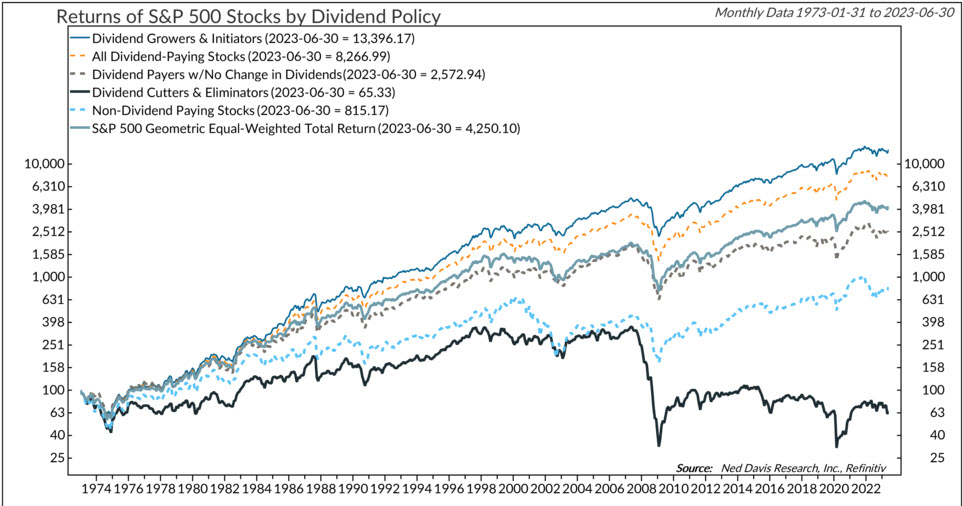

A recent study by Ned Davis Research shows that dividend growers tend to meaningfully outperform the market over time. This study has been updated through multiple economic and market cycles and consistently shows that dividend growers outperform.

Indices are unmanaged and not available for direct investment. For illustrative purposes only.

The Best of Both Worlds: Less Volatility, Higher Returns

Perhaps the most compelling attribute of companies with long histories of growing dividends is the fact that these businesses tend to exhibit attractive returns with less volatility over time. In fact, from January 1990 to June 2021, a basket of companies with the longest sustained histories of dividend growth both outperformed the broader S&P 500 index and saw less price volatility, resulting in a higher Sharpe ratio for the dividend paying basket. Specifically, the dividend paying basket outperformed significantly during drawdowns while performing roughly in line with the market during periods of broad advances in equities. This lower volatility outperformance is not a coincidence — we believe it results directly from the better underlying business performance and better balance sheets characterizing these companies.

Tying it Together

As always, we continue to seek investment opportunities in great or improving businesses at attractive valuations and inflection points. Emphasizing companies that pay growing dividends and have a long history of doing so is just another flavor of that approach, and we view the current market environment as ripe with opportunities in this area.

Nael Fakhry

Co-Chief Investment Officer – Core Equity

Featuring

Nael Fakhry

Co-Chief Investment Officer – Core Equity

Nael Fakhry, a partner at Osterweis, is a Portfolio Manager for the core equity, growth & income, quality cyclical growth, and flexible balanced strategies. He loves the process of researching companies and studying the history of various industries.

Prior to joining Osterweis Capital Management in 2011, Nael worked as an Associate at American Securities, a private equity firm, and as an Analyst in the investment banking division of Morgan Stanley.

Nael graduated from Stanford University with a B.A. in History, Phi Beta Kappa and the University of California Berkeley, Walter A. Haas School of Business with an M.B.A., where he was a C.J. White Scholar. Outside of his professional life, Nael enjoys coaching his kids’ soccer and basketball teams, reading, and running. He also contributes to the community as Treasurer and member of the Board of Directors of the Burlingame Community Education Foundation, where he supports local education and helps manage the endowment.

For more information about this strategy, please send us an email or call us at (800) 700-3316.

Related Insights

The Osterweis Funds are available by prospectus only. The Funds’ investment objectives, risks, charges, and expenses must be considered carefully before investing. The summary and statutory prospectuses contain this and other important information about the Funds. You may obtain a summary or statutory prospectus by calling toll free at (866) 236-0050, or by visiting www.osterweis.com. Please read the prospectus carefully before investing to ensure the Fund is appropriate for your goals and risk tolerance.

Investing involves risk. Principal loss is possible.

Diversification does not assure a profit, nor does it protect against a loss in a declining market.

The S&P 500 Index is an unmanaged index that is widely regarded as the standard for measuring large-cap U.S. stock market performance.

Free cash flow represents the cash that a company is able to generate after laying out the money required to maintain and expand the company’s asset base. Free cash flow is important because it allows a company to pursue opportunities that enhance shareholder value.

The Sharpe Ratio represents the added value over the risk-free rate per unit of volatility risk.

Yield is the income return on an investment, such as the interest or dividends received from holding a particular security.

Osterweis Capital Management is the adviser to the Osterweis Funds, which are distributed by Quasar Distributors, LLC. [OSTE-20230710-0923]